Working Paper Series no. 710: Investment and the WACC: new micro evidence for France

We exploit a new dataset of consolidated balance sheets for some 1,850, mostly nonlisted, French corporate groups, in order to investigate the relationship between corporate investment and the cost of capital. Our empirical model is motivated by a standard Q-theory of investment and relates the rate of investment to a proxy for profits, the cost of capital and firm- and sector-level controls. We notably construct firm-level measures of the weighted average cost of capital (WACC) that account for industry-specific values of the cost of equity and reflect the actual capital structure of firms. We find a confirmation that a high WACC drags down investment: a one SD increase in the real WACC (+2 pp) is associated on average with a reduction by 0.65 pp in the investment rate. The effect is somewhat larger for manufacturing firms and when firms are highly leveraged or more dependent on external finance. We also investigate the impact of lower competition or higher uncertainty on business investment and do not find evidence in support of any role of these two factors in France in recent years..

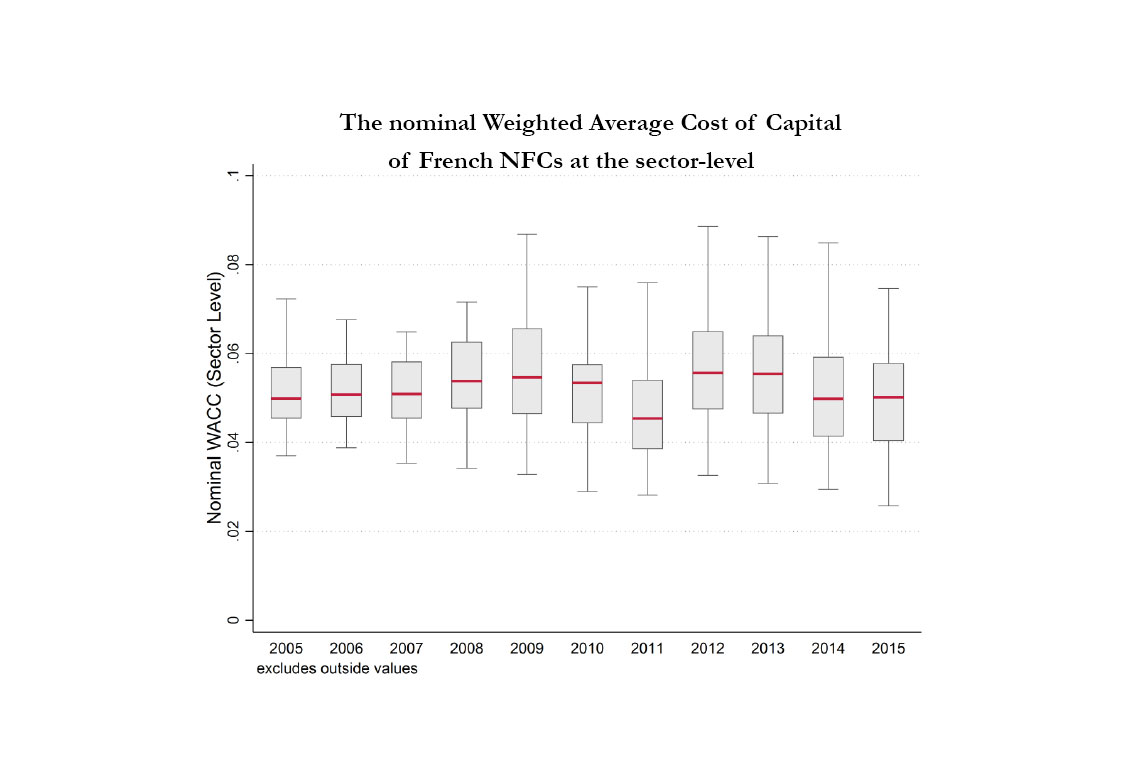

The weighted average cost of a firm’s capital (WACC) is a widely used benchmark for assessing investment opportunities in practice. Survey evidence suggests that a large majority of firms rely on net present value techniques for capital budgeting and that many firms use a firm-level WACC to discount the future cash flows derived form a new investment. However, as firm-level WACC are in general not observable by researchers, empirical evidence of how corporate investment reacts to the WACC is scarce and most studies exploiting firm-level panel data proxy their cost of capital by some interest rate, thereby ignoring the role of the cost of equity (COE) in firms’ capital formation decisions. This is inadequate as most firms fund their investments using a mix of equity and debt and the individual WACC may diverge sensibly from a firm’s cost of debt. Recently, some observers have indeed blamed “excessive” levels of corporates’ COE for the persistent sluggishness of productive investment in developed economies after the 2008 crisis in spite of central banks’ success in driving down nominal interest rates to very low levels.

In this paper, we assess the impact of the WACC on corporate investment using new firm-level data for some 1,850 French, mostly non-listed, non-financial corporate groups from 2005 to 2015. We motivate our empirical model by referring to a standard Q-model of investment, where Tobin’s Q appears to be negatively correlated to the firm’s WACC. We construct firm-level measures of the WACC that incorporate estimates of the COE based on industry-specific stock market information and a standard dividend-discount model. Controlling for all potentially relevant firm- and sector-level factors, we find new evidence that fluctuations in a firm’s WACC matters for investment, notably in the manufacturing sector and for larger firms. Yet, the evidence suggests that the negative impact of the WACC remains contained: a one SD increase in the real WACC (+2 pp) is associated on average with a reduction by 0.67 pp in the investment rate (5% of its average value). Furthermore, we show that financially more fragile firms or firms that rely more on external finance appear to cut investment more when facing an increase in their cost of capital.

Additionally, our analysis provides useful benchmarks for macroeconomic investment modelling and policy analysis. In particular, this paper relates to the ongoing debate about the causes of the sluggish rate of corporate investment observed in many developed economies in the aftermath of the 2008 crisis. According to our results subdued corporate investment in France over recent years can be traced back to a lower profitability, presumably reflecting depressed demand, and a high cost of capital.

Download the PDF version of this document

- Published on 03/05/2019

- 28 pages

- EN

- PDF (3.78 MB)

Updated on: 03/05/2019 15:26