Working Paper Series no. 826: A “Silent Spring” for the Financial System? Exploring Biodiversity-Related Financial Risks in France

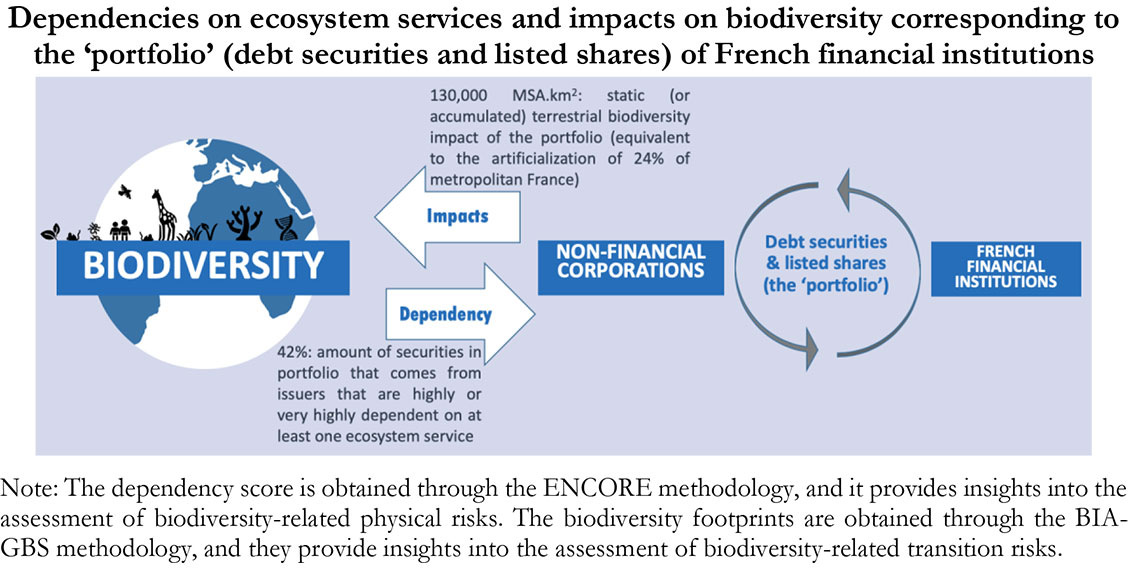

This paper contributes to an emerging literature aimed at uncovering the linkages between biodiversity loss and financial instability, by exploring biodiversity-related financial risks (BRFR) in France. We first build on previous studies and propose an analytical framework to understand BRFR, emphasizing the complexity involved and the limited substitutability of natural capital. We then provide quantitative estimates of dependencies and impacts of the French financial system on biodiversity. We find that 42% of the value of securities held by French financial institutions comes from issuers that are highly or very highly dependent on one or more ecosystem services. We also find that the accumulated terrestrial biodiversity footprint of these securities is comparable to the loss of at least 130,000 km² of “pristine” nature, which corresponds to the complete artificialization of 24% of the area of metropolitan France. Finally, we suggest avenues for future research through which these estimates could feed into future assessments of physical and transition risks.

Biodiversity is the living fabric of our planet, yet it is facing a massive decline caused by human activities. The risks posed by biodiversity loss to ecological and socioeconomic systems could be at least as high as those imposed by climate change, in addition to interacting with them. In this context, the financial community recently started paying attention to biodiversity-related financial risks (BRFR): as BRFR could pose a threat to financial stability, it has become increasingly important for central banks and financial supervisors to better understand such risks. However, a wide range of challenges, including the complexity of ecosystem processes and the limited substitutability of ‘natural capital’, makes assessing BRFR even more complex than assessing climate-related financial risks.

Against this backdrop, we build on van Toor et al.’s (2020) pioneering study in the Netherlands to provide the first exploration of BRFR for the French financial system. Based on data of the debt securities and listed shares issued by non-financial corporations and held by French financial institutions (the ‘portfolio’), we proceed as follows.

To approximate physical risks, we provide a measure of the dependencies of the economic activities financed by French financial institutions to a list of 21 ecosystem services. Considering the direct dependencies: we find that 42% of the market value of securities held by French financial institutions comes from issuers (non-financial corporations) that are highly or very highly dependent on at least one ecosystem service. Considering the upstream (or indirect) dependencies to ecosystem services, we find that all security issuers in the portfolio are at least slightly dependent to all ecosystem services through their value chains.

To approximate transition risks, we provide measures of impacts on terrestrial and freshwater (i.e. not marine) biodiversity of economic activities financed by French financial institutions (i.e. the “biodiversity footprint” of their portfolio). We find that the accumulated (or static) terrestrial biodiversity footprint of the French financial system is comparable to the loss of at least 130,000km² of ‘pristine’ nature, which corresponds to the complete artificialization of 24% of the area of metropolitan France. Land use change is the main pressure explaining these results. Moreover, the portfolio of French financial institutions has an annual additional (or dynamic) impact on terrestrial biodiversity that is comparable to the loss of 4,800km² of ‘untouched’ nature, corresponding to an annual complete artificialization of 48 times the area of Paris. Climate change is the main pressure explaining these results.

Lastly, we suggest future avenues of research consisting in: (i) developing biodiversity-related scenarios tailored to financial risk assessment; (ii) using specific methodologies that can better capture the limited substitutability of ecosystem services and the nonlinear patterns that their disruption could generate; and (iii) developing new tools through which the alignment of financial institutions with biodiversity-related goals could be assessed.

Download the PDF version of this document

- Published on 08/27/2021

- 95 pages

- EN

- PDF (3.69 MB)

Updated on: 08/27/2021 17:23