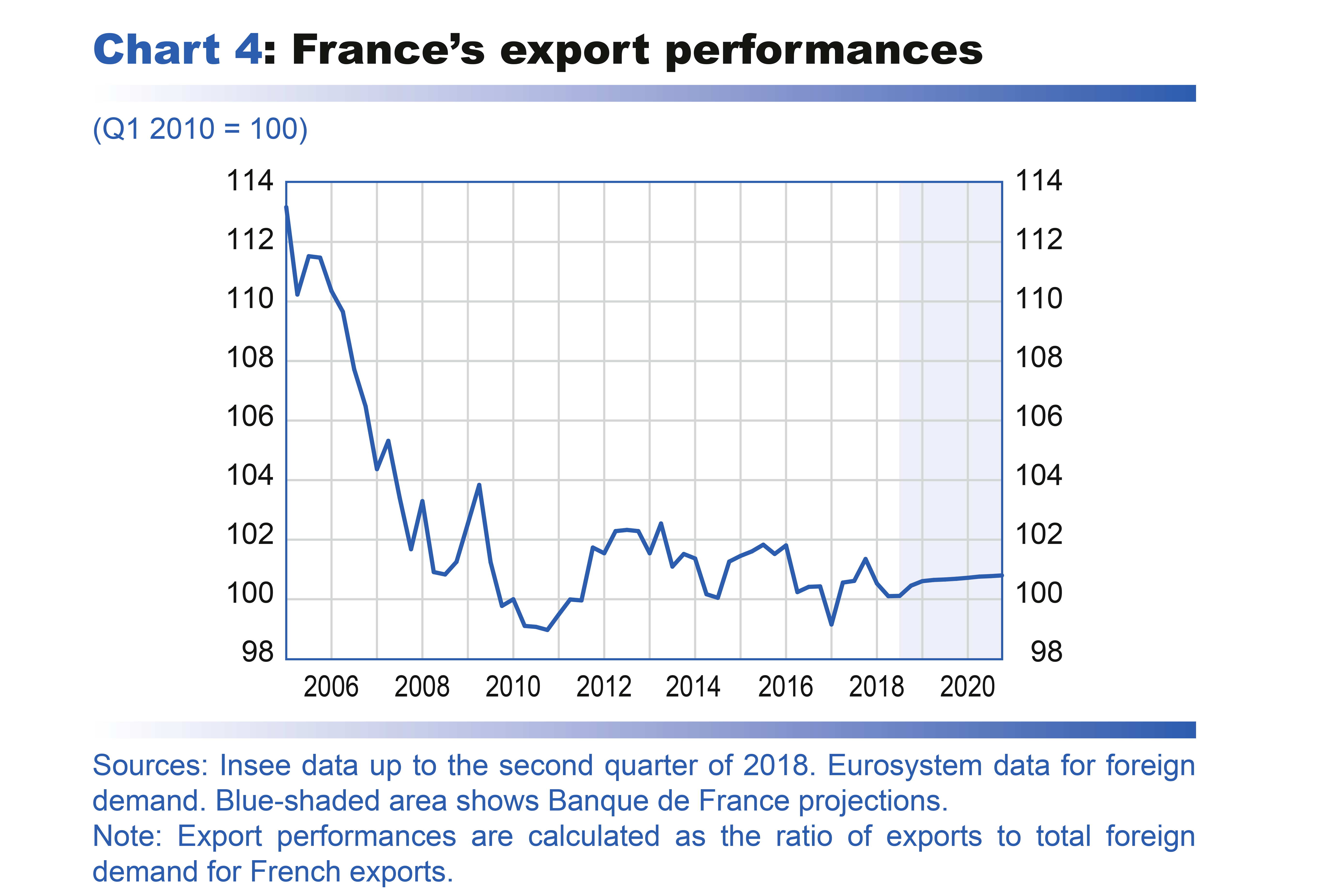

The switch to a 2014 base in the national accounts has resulted in significant revisions to household gross disposable income (GDI). These mainly reflect adjustments to net flows of financial income (dividends and interest), as Insee has reviewed its methodology for estimating these items and now notably takes into account tax data on resident households (see “The national accounts switch to a 2014 base ” and “France’s current account deficit and borrowing requirement compiled using a 2014 base”, French version only , May 2018).

These changes have led to a significant downward revision to the saving ratio up to 2005 (see Chart A). As a result of this new historical data, the saving ratio for end 2017 is no longer as low as it was using the 2010 base. Moreover, the saving ratio follows a hump shaped trajectory from 2009 to 2013, and appears particularly high during that period. All of this raises questions as to the medium term outlook for the saving ratio in our projections.

The major revisions to the data have led us to estimate a new equation for consumption (for a description of the previous specification used, see Faubert, V. and Olivella Moppett, V. 2015, “How can the rise in the French household saving ratio since the start of the crisis be explained?”, Rue de la Banque, No. 9, September). The previous equation was based on the assumption that, beyond its near term fluctuations, consumption evolved in a manner that allowed the saving ratio to revert towards its long run target. In the new equation, this long term pattern has been modified. The chosen specification, inspired by Bonnet and Poncet (see Bonnet, X. and Poncet, H. 2004, “Structures de revenus et propensions différentes à consommer ”, [Structure of income and different propensities to consume], Insee Working Paper, December), incorporates two new features.

- First, over the long run, consumption depends on the level of disposable income excluding net financial income (net financial income = net interest earned + net dividends earned + other net income (income distributed to insurance policyholders, rental income from land) and no longer on total GDI. As a result, the saving ratio, which is a function of total GDI, may vary depending on changes in the weight of net financial income.

- Second, the proportion of household GDI (excluding net financial income) that is actually consumed depends on the composition of that income, and in particular on: (i) the share of gross wages (excluding employer social security contributions) and social security benefits; and (ii) the share of gross operating surplus from the self employed.

The inclusion of variables linked to the composition of GDI is based on the assumption that marginal propensities to consume differ according to the income source. In our estimated equation, a shock to labour income or benefits, assuming other income remains stable, is consumed nearly in full, leaving the saving ratio almost unchanged. Conversely, in the case of a reduction in direct taxes and social security contributions, half of the gains are spent while the rest are saved, resulting in a rise both in consumption and in the saving ratio. A cut of 1 percentage point in the share of direct taxes and social security contributions in GDI leads, all else being equal, to a 0.3 percentage point rise in the saving ratio over the long run. In the case of net financial income, the estimates suggest that the marginal propensity to consume is close to zero, so shocks to this income only affect the saving ratio.

In the new model, the speed of adjustment of consumption to its long run determinants – allowing a stabilisation of the share of income consumed – is much higher than in the equation without composition effects. In general, following a shock to real GDI (excluding net financial income) but with no change in income structure, 60% of the consumption adjustment has occurred after around one year, compared with 50% in the previous equation.

The new equation also more accurately reproduces the actual saving ratio observed since 2005 (see Chart B). There is no longer an overestimation bias from 2002 to 2008 as there was with the previous equation, and the hump shaped pattern from 2009 to 2013 is adequately explained by the equation’s determinants. Indeed, the ratio’s trajectory from 2009 to 2013 is attributable to two separate effects: (i) in 2008, the share of gross operating surplus from the self employed declined, leading to a rise in the saving ratio; and (ii) in 2012, the sharp increase in direct taxes and social security contributions led to a decline in the saving ratio. In the recent period, the simulated saving ratio is only slightly higher than the actual one, reflecting the ongoing decline in the share of gross operating surplus from the self employed in household GDI.

Over the projection horizon, the structure of household GDI is expected to be strongly impacted by the planned cuts to direct taxes and social security contributions. Direct taxes and social security contributions are projected to decline by 1.3 percentage point as a share of GDI between 2017 and 2020, which should help to boost consumer spending. However, in line with our previous estimates, a portion of the gains are expected to be saved, resulting in an increase in the saving ratio of around 0.5 percentage point from 2017 to 2020 in our projections.

Obviously, there are still some uncertainties surrounding the estimated saving ratio for 2020. The change in the structure of GDI could have a stronger than expected impact, leading to a higher saving ratio and therefore lower consumption and GDP levels than in our baseline scenario. Conversely, it could have a lower than expected impact, with the saving ratio falling back towards its long term average (average of 14.5% between 1995 and 2017), which in turn would lead to higher than projected consumption and GDP.