Macroprudential policy instruments: a bulwark against interbank contagion risk

Financial institutions are connected among themselves through multiple contracts: loans, bilateral security holdings, derivatives contracts, etc. In normal times, these relationships allow for risk-sharing. However, in times of stress, they turn into channels of shock propagation, through solvency default cascades, funding shortages and asset-fire sales.

Macroprudential policy aims to mitigate these effects using different instruments, such as higher capital surcharges for systemic institutions.

Public authorities monitor in particular financial interconnections by exploiting information on the bilateral relationships between financial institutions. They notably take these elements into account in the stress tests applied to the entire financial system.

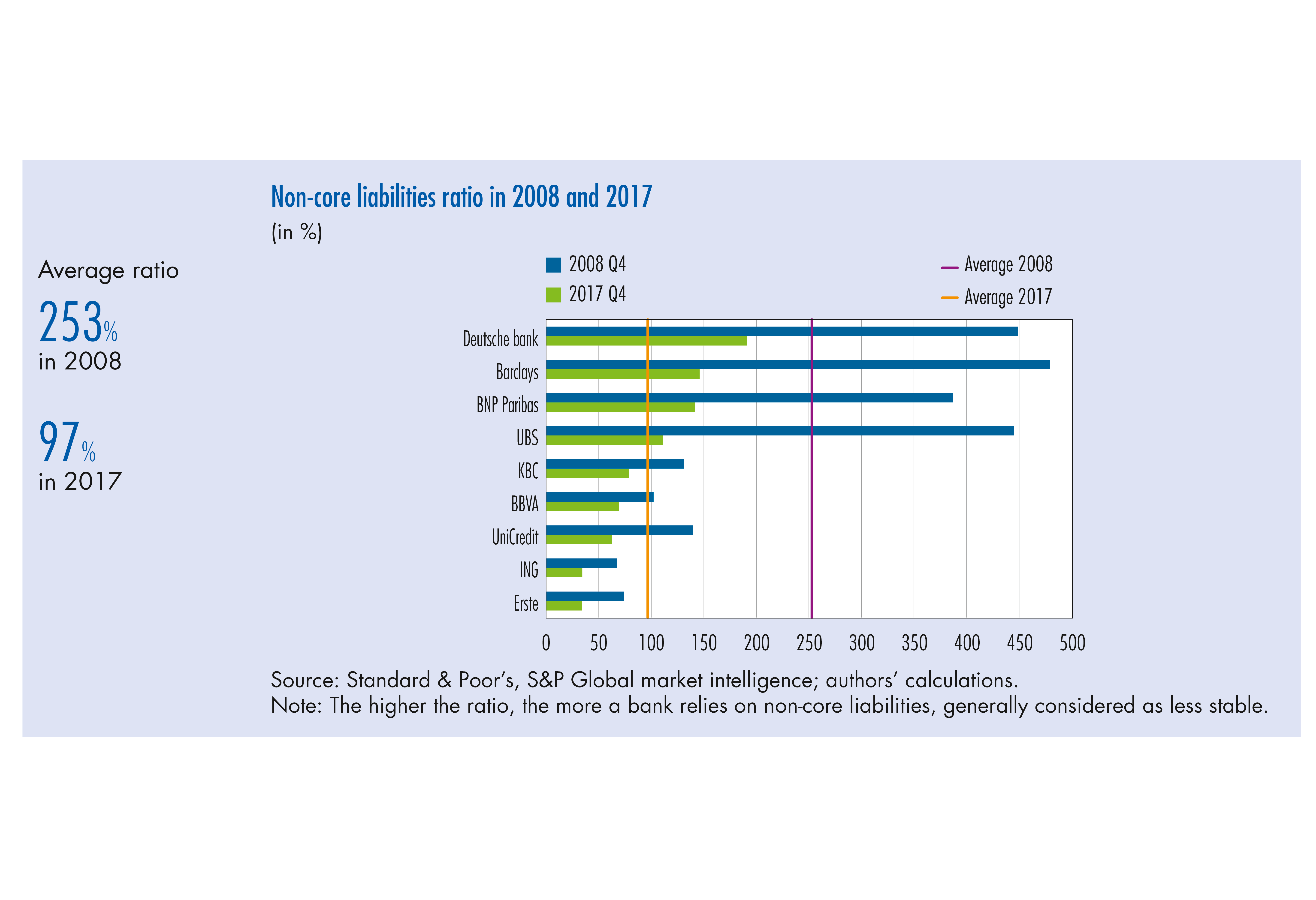

The 2008 financial crisis underlined the interconnected nature of the financial system, which significantly contributed to spreading stress through the system. Financial institutions are linked to each other through multiple contracts, such as loans, stock and bond holdings, derivative contracts as well as through holdings of common assets. When a market shock hits a financial institution, losses suffered by this firm may spread to others connected to it; the latter in turn may transmit this shock to their counterparties, and so on. There are several channels through which an initial shock is propagated and amplified.

All these channels were present to differing extents during the recent crisis and played a role in the amplification of initial shocks. In response to these risks, public authorities have implemented macroprudential instruments that aim to monitor risks related to financial interconnections, improve the resilience of the financial system and mitigate channels of shock amplification.

1 Shock propagation between financial institutions

Shock transmission mechanisms

A stylised balance sheet displays the links between institutions in order to better understand the shock transmission mechanisms. On its asset side, a bank has assets external to the interbank system and interbank short‑ and long‑term assets. External assets correspond to marketable securities, which can be traded on the secondary market, such as sovereign bonds, stocks and bonds of non‑financial corporations, and non‑marketable assets, such as loans to households and firms. Interbank assets correspond to loans and security holdings (bonds, stocks, etc.) issued through financial institutions. The liability side has a similar structure with external liabilities that correspond to obligations to non‑financial entities, such as deposits. The difference between assets and liabilities is equity.

The first transmission channel is direct exposure or solvency cascades: this can occur in two ways. First, banks exposed to their defaulted counterparty through long‑term loans suffer a loss equal to their exposure amount corrected by a recovery rate. Second, falls in the price of securities (stocks and bonds issued by banks) may affect other banks via their direct exposure: for example, if bank A directly holds stocks (or bonds) issued by bank B. In this case, banks may suffer losses even in the absence of counterparty default as a result of the fall in the price of these marked‑to‑market securities. These loans and cross‑holdings of marketable securities are classified as interbank assets in the balance sheet above.

Télécharger la version PDF du document

- Publié le 26/09/2018

- 8 page(s)

- EN

- PDF (277.61 Ko)

Bulletin Banque de France 218

Mis à jour le : 30/10/2019 18:38